What are the three main barriers to overcome for a successful MBO?

17th Jan 2019

Succession is a difficult bridge to cross in the life of a business owner. For businesses which have a management team who are not the owners, a Management Buyout (‘MBO’) can become an attractive avenue for all parties involved.

From our perspective there are three main challenges which need to be overcome to ensure a successful MBO. These are the price, how it will be funded and any obstacles in the Company’s governing documents.

Although these may sound like formidable hurdles, early professional input can help identify the potential crunch points to ensure these areas are discussed and agreed at the outset.

1. Price

This is likely to be the initial area of contemplation for both the Seller and the MBO Team. Ultimately if the embryonic view of the price begins too far apart then the chances of a successful deal are much reduced. It is therefore vital that the expectations are managed on both sides at the outset.

Many people we speak to are surprised to hear that there is no set price formula which must be adhered to. Professional business valuations are designed using various methodologies which include a degree of subjective input. Fundamentally the value of any asset is the intersection of the amount where a Seller is willing to sell and a buyer is willing to buy.

When setting a price, it is important that the Seller looks beyond the headline price to see the full benefits of striking a deal. In a lot of cases this will involve obtaining Entrepreneurs Relief on their proceeds. This means that a Seller ‘cashes out’, receiving their proceeds and paying a tax rate of only 10%, as opposed to extracting surplus cash as dividends which currently could entail a tax rate of up to 38.1%.

2. Funding

The subject of funding will clearly have an impact on the price which the MBO Team is able to offer for the business. It is essential that a prospective MBO Team realise that it would be extremely unusual for such a purchase to be fully paid out of their own pockets on day one.

Most MBOs will be funded by a mixture using some of the following:

A chunk of the amount payable to the Seller will usually be deferred over an agreed period to avoid putting too much strain on the business. Sellers are usually not averse to this as it allows them to retain a connection with the business and possibly earn interest on the outstanding amount.

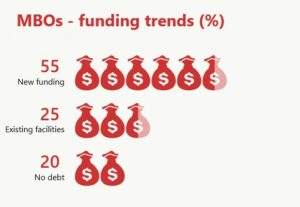

80% of the MBOs which we have advised on in the last 2 years have included funding from lenders, either from new funding lines or by increasing the drawdown from existing facilities.

The majority of this funding will be achieved by securing debt against the assets which the Company owns. The structure of the balance sheet will be an important consideration when assessing whether an MBO is feasible.

Funders will typically want the MBO Team to have a financial stake in the business, whether through introduced funds or charges/guarantees held against personal assets.

3. Legals

When designing an MBO structure, a review of the Company’s governing documents should not be neglected. It is not unusual for a shareholders agreement or the articles of association to include a clause with the ability to derail an MBO.

If the current shareholders are all supportive of the MBO then it is likely that potential barriers such as restrictions on issuing or selling shares, or a stipulated share value can be overcome with early identification. If any restructuring is required, it becomes especially important to identify this early as it may take another two years for the Sellers to be entitled to Entrepreneurs Relief after any restructuring.

A more problematic barrier would be if EMI share options have been issued which crystallise on the sale or partial sale of the business. In this instance, hopefully the EMI option holders would all be part of the MBO Team, making waiving the rights easier. If an EMI holder were not part of the MBO Team then this area would require careful consideration at the very outset of the potential transaction.

Summary

MBOs tend to lend themselves to more collaborative negotiations than trade sales, however it is important that the fundamental areas are reviewed and agreed at the outset of any project. Ensors Corporate Finance team are experienced in advising on MBOs and feel that we can add value and make the process more efficient by being involved from the outset.

For more information please contact Simon Martin.